The Post Office RD Scheme stands out as one of the safest and most accessible investment options for individuals looking to build a substantial fund through monthly savings. Many investors wonder about the potential returns when depositing ₹12,000 monthly in a Post Office Recurring Deposit for five years. With the current interest rate structure, this investment strategy yields impressive results, offering a maturity amount of approximately ₹8,56,388 against a total investment of ₹7,20,000.

How Does Post Office RD Work?

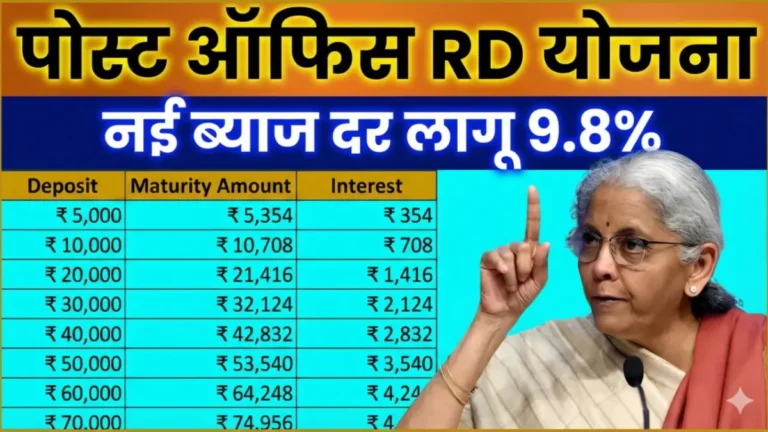

The Post Office Recurring Deposit operates on a five-year tenure with a current annual interest rate of 6.7%. This interest compounds quarterly, maximizing your returns over time.

Each monthly installment earns interest based on its deposit duration. Therefore, earlier deposits accumulate interest for the full five years, while later deposits earn proportionally less interest until maturity. This compounding mechanism transforms regular monthly contributions into a substantial corpus.

Complete Calculation of ₹12,000 Monthly RD for 5 Years

When you deposit ₹12,000 monthly in a Post Office RD, your total principal investment over 60 months amounts to ₹7,20,000. However, with the 6.7% annual compounding interest, the maturity value reaches approximately ₹8,56,388.

This means you earn approximately ₹1,36,388 as interest over the five-year period. The power of compounding transforms this seemingly modest monthly saving into a significant fund that grows exponentially over time.

Who Should Consider ₹12,000 Monthly RD Investment?

This investment amount suits individuals with stable income streams who want to develop disciplined saving habits. Furthermore, it’s ideal for salaried professionals, small business owners, or anyone preparing for future major expenses.

Additionally, risk-averse investors who prefer guaranteed returns over market volatility find Post Office RD particularly attractive. The scheme offers peace of mind with principal protection and assured interest rates.

Why Do People Prefer RD’s Safety Features?

Post Office operates under complete government guarantee, ensuring absolute security of your invested capital. Moreover, the fixed interest rate provides predictability, allowing you to calculate exact maturity proceeds in advance.

This reliability factor makes the scheme appealing to millions of investors who prioritize capital preservation over higher but uncertain returns. Consequently, families can plan their financial future with confidence.

Can You Close RD Before Maturity?

Yes, you can close your RD before the five-year maturity period if needed. However, premature closure results in reduced interest rates, typically aligned with savings account rates.

Therefore, it’s advisable to maintain the RD for the complete tenure to maximize compounding benefits. This approach ensures you receive the full advantage of the higher interest rate structure.

How Can This Fund Be Utilized After 5 Years?

The ₹8.56 lakh corpus becomes extremely versatile for various financial needs. Investors commonly use this amount for home renovations, children’s education fees, vehicle down payments, or small business ventures.

Additionally, this risk-free accumulated wealth provides financial security and flexibility for unexpected expenses or planned major purchases. The substantial amount creates multiple opportunities for wealth deployment.

Tax Benefits and Considerations

Post Office RD offers certain tax advantages under Section 80C of the Income Tax Act. However, the interest earned is taxable as per your income tax slab.

Nevertheless, the guaranteed returns and government backing often outweigh the tax implications for conservative investors. Therefore, consult with tax advisors for optimal tax planning strategies.

Frequently Asked Questions

What is the minimum amount required to start a Post Office RD?

The minimum monthly deposit for Post Office RD is ₹100, while there’s no maximum limit. You can choose any amount based on your financial capacity and investment goals.

Can I increase my monthly RD amount mid-term?

No, you cannot increase the monthly deposit amount in an existing RD account. However, you can open multiple RD accounts with different monthly amounts if needed.

What happens if I miss a monthly RD payment?

Missing payments attracts a penalty fee, and your account may become irregular. It’s important to maintain timely payments to avoid complications and ensure smooth maturity.

Is Post Office RD better than bank RD schemes?

Post Office RD typically offers slightly higher interest rates compared to most bank RDs. Additionally, government backing provides superior security compared to private sector alternatives.

Can NRIs invest in Post Office RD schemes?

No, Non-Resident Indians (NRIs) are not eligible to invest in Post Office RD schemes. These schemes are exclusively available for Indian residents only.

Disclaimer: This article is written for general information purposes only. Interest rates may change over time, so please check the latest interest rates and terms with your nearest post office before investing. This does not constitute financial advice.