Building a substantial fund for the future through Post Office RD Scheme has become one of the most accessible and secure investment options available today. Many people start with small savings, while others invest larger amounts like ₹12,000 monthly to achieve bigger financial goals. The question frequently asked is how much return one can expect from a 5-year RD of ₹12,000 per month. The calculation based on current Post Office interest rates reveals fascinating results.

How Does Post Office RD Work?

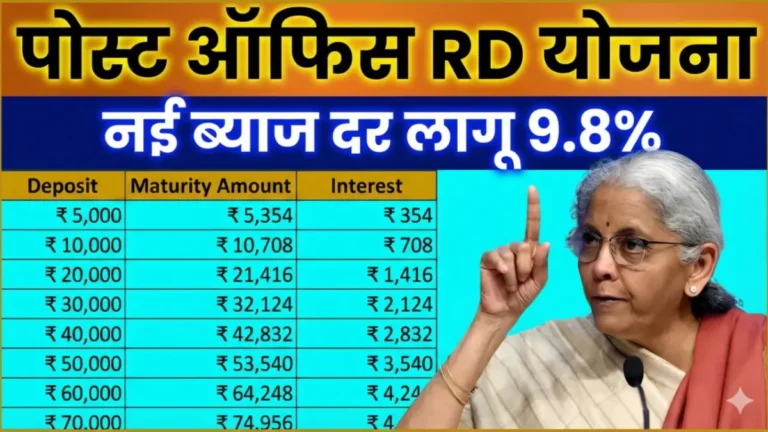

The Post Office RD operates with a 5-year tenure and currently offers 6.7% annual interest. This interest compounds quarterly, which significantly boosts your returns over time.

When you deposit the same amount every month, each installment earns interest based on its duration in the account. Therefore, early deposits earn interest for the full 5 years, while later deposits accumulate slightly less interest before maturity.

This systematic approach ensures that your total maturity amount becomes substantially larger than your principal investment, demonstrating the power of consistent savings combined with compound interest.

Complete Calculation for ₹12,000 Monthly RD Over 5 Years

When you deposit ₹12,000 monthly in Post Office RD, your total principal investment over 60 months equals ₹7,20,000. This represents the actual money from your pocket.

However, when the 6.7% annual compounding interest is added, the maturity amount reaches approximately ₹8,56,388. This means you earn a total interest of around ₹1,36,388.

What appears to be simple monthly savings transforms into a significant fund through compound interest. Moreover, this demonstrates the true power of RD where consistent small investments grow into substantial wealth over time.

Who Should Consider ₹12,000 Monthly RD?

Many families choose to allocate a portion of their monthly income to secure savings through RD. This amount particularly suits individuals with stable income who want to develop a disciplined saving habit.

Whether you’re a salaried employee, run a small business, or preparing for future major expenses, this savings plan can prove highly beneficial. Furthermore, it’s perfect for those who fear market volatility or prefer not to take risks with stock market investments.

Post Office RD offers the most comfortable and reliable option where your money remains safe while earning guaranteed returns.

Why Do People Prefer RD Security?

Post Office operates under complete government guarantee, ensuring that every rupee of your principal amount remains absolutely secure. Additionally, the interest rate remains stable, allowing you to know exactly how much you’ll receive at maturity.

This reliability makes the scheme special, and millions of people secure their future by depositing small amounts monthly in RD. The government backing provides unmatched peace of mind for conservative investors.

Can You Close RD Before Maturity?

If necessary, you can close your RD before maturity, though the interest earned will be slightly reduced. Post Office adjusts the deposited amount according to savings account interest rates.

Therefore, it’s advisable to let your RD run for the complete 5-year term to gain maximum benefit from compounding. Early withdrawal significantly reduces your overall returns.

How This Fund Helps After 5 Years

People who maintain a ₹12,000 monthly RD develop a robust fund of approximately ₹8.56 lakh after 5 years. This amount proves helpful for home repairs, children’s education fees, car down payments, starting a small business, or any major expense.

Without any risk or hassle, this amount available after 5 years can prove extremely useful for various life goals. The predictable nature of returns makes financial planning much easier.

Tax Benefits and Additional Advantages

Post Office RD offers certain tax advantages under specific conditions, making it even more attractive for investors. The interest earned is subject to tax, but the principal amount enjoys safety guarantees.

Additionally, the scheme allows for easy loan facilities against your RD account after completing certain tenure requirements. This feature provides liquidity without breaking your investment.

Frequently Asked Questions

What is the minimum amount required to start Post Office RD?

You can start Post Office RD with as little as ₹100 per month. The maximum limit is ₹1.5 lakh per month, allowing flexibility for different income groups.

Can I increase my monthly RD amount mid-term?

No, you cannot increase the monthly deposit amount once the RD is started. However, you can open multiple RD accounts with different amounts if needed.

What happens if I miss a monthly installment?

Missing installments attracts a penalty charge. You’ll need to pay the missed amount along with applicable penalties to keep your account active and maintain the benefits.

Is the 6.7% interest rate guaranteed for the entire tenure?

Yes, once you open the RD account, the interest rate applicable at that time remains fixed for the entire 5-year tenure, regardless of future rate changes.

Can I withdraw money from RD in case of emergency?

Yes, premature withdrawal is allowed after completing one year, but you’ll receive reduced interest rates and may face penalty charges depending on the withdrawal timing.

Disclaimer: This article is written for general information purposes only. Interest rates may change over time, so please check the latest interest rates and rules with your nearest Post Office before investing. This is not financial advice of any kind.