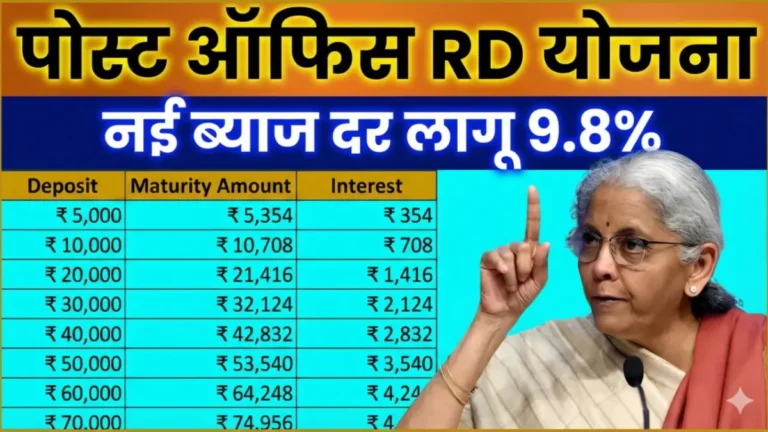

Post Office RD Yojana offers a secure monthly savings option where depositing ₹13,000 monthly can yield ₹9,27,753 after 5 years. This government-backed scheme provides guaranteed returns without market risks, making it ideal for salaried individuals and small business owners seeking steady wealth creation. The scheme operates on a 6.7% annual interest rate with quarterly compounding, ensuring your money grows consistently over time.

How Post Office RD Scheme Works

The Post Office Recurring Deposit runs for 5 years or 60 months. Currently, the scheme offers approximately 6.7% annual interest, compounded quarterly. This means each monthly installment earns interest for different durations.

Money deposited earlier earns interest for a longer period, while later deposits accumulate interest for shorter durations. However, all installments combine to create a substantial fund after 5 years. Since this is a completely government scheme, your deposited money remains entirely secure.

Total Investment with ₹13,000 Monthly Deposits

When you deposit ₹13,000 monthly in Post Office RD, your total investment over 5 years becomes ₹7,80,000. This represents the actual amount you save from your pocket gradually over time.

The real benefit begins when quarterly compound interest gets added to this amount, making your fund grow rapidly. Therefore, the power of compounding transforms your regular savings into substantial wealth.

How ₹9,27,753 Maturity Amount is Calculated

Now comes the calculation every investor wants to understand. With a 6.7% annual interest rate, running an RD of ₹13,000 for 60 months yields approximately ₹9,27,753 at maturity.

Your total deposited amount equals ₹7.8 lakh, but compound interest adds approximately ₹1,47,753 as additional earnings. This entire benefit comes from compounding, making RD a powerful method for transforming small savings into large funds.

Furthermore, the quarterly compounding ensures that interest earned also starts earning interest, maximizing your returns over the investment period.

Who Should Consider ₹13,000 RD Investment

This investment suits people with stable income who can comfortably set aside a fixed amount monthly. Salaried employees, small business owners, and families preparing for future major expenses find this plan extremely useful.

Moreover, it involves no significant risk or complexity. You simply deposit a fixed amount monthly, and the fund grows automatically over time. Additionally, the government backing provides complete security for your investment.

Practical Uses for ₹9.28 Lakh Fund After 5 Years

The approximately ₹9.28 lakh fund received after 5 years can serve multiple purposes:

- Children’s education expenses

- Home renovation projects

- Down payment for new vehicle

- Business expansion capital

- Emergency financial requirements

Many investors reinvest this amount in other secure schemes to further grow their wealth. However, Post Office RD’s main advantage is preparing you for the future without any risk.

Impact of Premature RD Closure

If circumstances force you to close the RD before maturity, Post Office allows this facility. Nevertheless, premature closure may result in slightly reduced interest rates.

Therefore, it’s better to let the RD run for the complete 5 years. This ensures you receive the full benefit of compound interest and your fund reaches its maximum potential.

Key Benefits of Post Office RD Scheme

The scheme offers several advantages that make it attractive for conservative investors:

- Government guarantee ensures complete safety

- Quarterly compounding maximizes returns

- Flexible monthly installments

- Tax benefits under certain conditions

- No market-related risks

Additionally, the scheme helps develop disciplined saving habits while building substantial wealth over time.

Frequently Asked Questions

What is the current interest rate for Post Office RD?

Post Office RD currently offers approximately 6.7% annual interest rate, compounded quarterly. However, interest rates may change periodically based on government policies.

Can I deposit more than ₹13,000 monthly in Post Office RD?

Yes, Post Office RD allows flexible monthly deposits. You can choose any amount that suits your budget and financial goals.

Is Post Office RD better than bank RD schemes?

Post Office RD typically offers competitive interest rates compared to banks, plus government backing provides additional security. However, compare current rates before deciding.

What happens if I miss a monthly installment?

Post Office provides some flexibility for missed installments with minimal penalty charges. However, regular deposits ensure maximum benefit from compounding.

Can I open multiple RD accounts in Post Office?

Yes, you can open multiple RD accounts with different amounts and tenures based on your investment strategy and financial planning needs.

Disclaimer: This article is written for general information purposes only. Post Office RD interest rates may change from time to time. Please check the latest interest rates and rules from your nearest post office before investing. This is not financial advice of any kind.